We are thrilled that for the sixth consecutive year, Experian has earned a score of 100 on the Human Rights Campaign Foundation’s (HRCF) 2025 Corporate Equality Index (CEI). This recognition underscores our commitment to LGBTQ+ workplace equality. We are honored to join the ranks of 765 U.S. businesses that have been awarded the HRCF’s Equality 100 Award, celebrating our leadership in fostering an inclusive workplace.

Experian’s dedication to supporting the LGBTQ+ community is reflected in several key initiatives:

- Name Change Process: We have a process for transgender and non-binary consumers to update their names on credit reports, ensuring their identities are accurately represented.

- LGBTQ+ Allyship 101 Training: This new training program is available to all Experian employees, promoting allyship and understanding within our workforce.

- Pride ERG Parenting Committee: Launched to support parents, grandparents and guardians of LGBTQ+ individuals, this committee provides valuable resources and community.

- Transgender Resource Guide: This guide supports employees who are transitioning at work, offering education and resources for colleagues and managers.

- Partnerships: We collaborate with organizations such as Out & Equal, GenderCool, The Trevor Project and Born This Way Foundation’s Channel Kindness to provide financial health, mental health and other resources to empower both our internal and external communities.

At Experian, we are proud to be part of this movement towards greater equality and inclusion. We remain dedicated to fostering a workplace where every employee feels respected, valued and empowered to bring their authentic selves to work.

Learn more about how we drive social impact in English, Portuguese and Spanish.

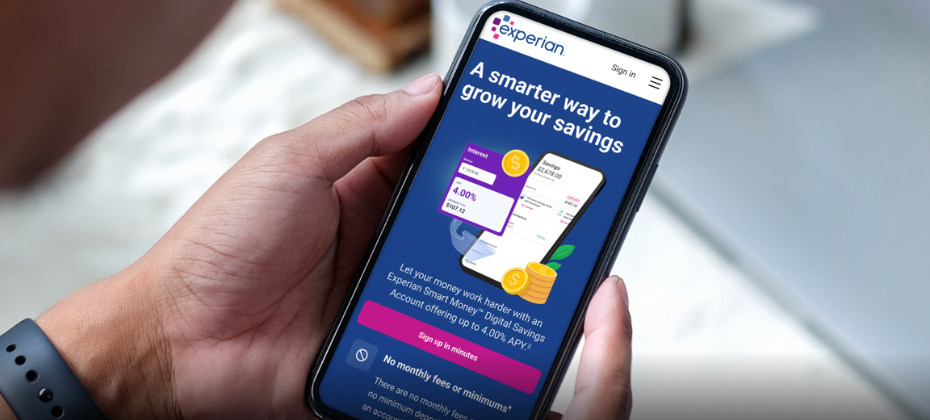

We’re starting the year strong by reaffirming our promise to empower consumers on their financial journeys. At Experian, everything we do is driven by our mission to bring Financial Power to All™—helping people not only understand where they stand but confidently move forward. That’s why I’m pleased to introduce the new high-yield Experian Smart Money™ Digital Savings Account[1], designed to make saving effortless, accessible, and more meaningful than ever before. This new offering is more than just a savings account—it represents an important evolution in how Experian supports financial progress. For years, we’ve helped tens of millions of consumers monitor their credit, improve their credit scores, and protect their identities. Now, by adding a high-yield digital savings account to our existing suite of financial health tools, we’re able to anchor that progress to something tangible: real balances and real momentum. With the ability to save built directly into the Experian ecosystem, members can track their savings growth alongside credit improvements, creating a clearer picture of their overall financial health. Positive financial behaviors—like paying down debt, making on-time payments, or improving utilization—can now be experienced in parallel with cash accumulation and stronger financial resilience, all in one trusted place. The Experian Smart Money™ Digital Savings Account offers up to 4.00% variable Annual Percentage Yield[2] (APY), which is nearly 10 times the national average savings rate[3], with no minimum balance or direct deposit requirement. It’s seamlessly integrated into the Experian membership experience, making it easier for consumers to take action the moment insight appears. This launch builds on the success of our Experian Smart Money™ Digital Checking Account & Debit Card introduced in 2023 and reflects our continued commitment to creating products that meet consumers wherever they are on their financial journey. We believe saving is a foundational financial behavior—and one that plays a powerful, often underappreciated role in credit outcomes. Strong credit health isn’t just about borrowing; it’s closely tied to liquidity, cash flow stability, and financial resilience. Having accessible savings can help consumers stay current on bills during income disruptions, build buffers that reduce reliance on higher-cost credit, and create flexibility that can support long-term credit improvement. In this way, a high-yield digital savings account becomes more than a place to store money—it becomes a practical tool for building healthier financial habits. Whether it’s emergency savings, goal-based saving, or smoothing cash flow, an Experian Smart Money Digital Savings Account enables consumers to turn good intentions into consistent action. This launch also reflects our broader evolution beyond a traditional credit bureau. Today, Experian membership provides access to credit monitoring and improvement tools, identity protection, a credit card marketplace, auto insurance comparison shopping, and personalized guidance through our AI-powered virtual assistant, EVA. Adding a high-yield digital savings account allows us to take the next step with our members—bridging the gap between insight and action. Instead of stopping at “here’s where you stand,” Experian can now help consumers actively build positive financial momentum. We’re extending our role as consumers’ BFF—Big Financial Friend—by making it easier to save, plan, and grow within the same ecosystem they already trust. By innovating and delivering products that truly make a difference in people’s everyday financial lives, we’re continuing to advance our mission and help consumers turn knowledge into progress. Learn more at experian.com/smartmoney. [1] The Experian Smart Money™ Debit Card is issued by Community Federal Savings Bank (CFSB), pursuant to a license from Mastercard International. Banking services provided by CFSB, Member FDIC. Experian is a Program Manager, not a bank. See Experian.com/legal. [2] The Annual Percentage Yield (APY) is 2.00%, 3.00% or 4.00% as of today’s date based on the Experian membership status. The APY may change at any time before or after your account is opened. Changes to the Experian membership can impact the APY, interest rate, and features. The interest rate and APY may be lower during membership trial periods. No minimum deposit to open account. Balance must be at least $0.01 to earn APY. Learn more. [3] As of Dec. 15, 2025, the national average rate for savings accounts was 0.39%, according to the FDIC.

The last several months stand out as one of the most dynamic periods in my career. To say it’s been an exciting time would be an understatement. For more than 20 years, the mortgage industry has relied on a single way to measure creditworthiness. With the Federal Housing Finance Agency’s decision to approve VantageScore 4.0 for use in mortgage decisions, that long-standing approach is evolving. At Experian, we’ve advocated for score choice in mortgage from the very beginning. We believe in modern scores because they allow more of Experian’s rich, differentiated data to be used in lending decisions. Because this data provides a more complete picture of a consumer’s financial health, it creates new opportunities to expand access to homeownership. At the same time, significant change naturally brings questions and debate. New models. New data sources. New decisions to make. New ways of doing things. Across the industry, there’s been a lot of discussion about what these changes mean in practice, how they impact lenders and consumers, and how the industry moves forward from here. I recently had the opportunity to talk through many of these topics with Robbie Chrisman on the Chrisman Commentary Daily Mortgage News Podcast. Our conversation focused on bringing clarity to some of the most common questions I’m hearing today, while also looking ahead to the opportunity in front of us: modernizing mortgage decisions in a way that reflects how consumers actually live and manage money to help more consumers realize their dreams of homeownership. We discuss the fundamentals, including the difference between credit reports and scores (and why that distinction matters), how expanded data, including things like rental data, cash flow insights and buy now, pay later information, can help lenders make more informed decisions and how we can help turn today’s renters into tomorrow’s homeowners. We separate fact from fiction on credit report pricing and we take a forward look at where we can, collectively as an industry, go from here. The good news is: Consumers haven’t stopped believing in homeownership. Our systems just need to continue evolving to reflect the way people live and manage money today. With better data and more modern tools, we are moving in the right direction. To hear more, listen to my full conversation with Robbie Chrisman on the Chrisman Commentary Daily Mortgage News Podcast.

At Experian, our mission is to bring financial power to all. That means breaking down traditional boundaries, creating pathways for those historically left out of the financial system, and working alongside organizations that share our commitment to inclusion. Credit Builders Alliance (CBA) is one of those partners. For years, CBA has connected community-based nonprofits with the major credit reporting agencies, helping credit-challenged consumers to build or rebuild credit – often for the first time. Our latest analysis done in partnership with CBA shows just how transformative this work can be. From unscored consumers reaching prime tiers to deep-subprime consumers seeing meaningful improvements, the data underscores a truth CBA has championed from the beginning: when people are given the opportunity to build credit, they use it to move forward. I recently had the opportunity to sit down with Dara Duguay, CEO of Credit Builders Alliance, to discuss these findings, the work her organization leads, and what’s needed to continue expanding access to fair, affordable credit for underserved communities. Q1: For those who may be unfamiliar, what is Credit Builders Alliance? Who do you serve and what role do you play in the financial ecosystem? Dara:Credit Builders Alliance is a national nonprofit network made up of community-based organizations, nonprofit lenders, and financial capability providers. Our mission is to help low- and moderate-income individuals and families build credit as an asset and gain access to the financial mainstream. We help nonprofits report loan repayment data to credit bureaus like Experian and we support organizations in strengthening their credit-building programs with training, tools, and technical assistance. Many of the consumers our member organizations serve start out with limited or no access to traditional financial products. Our work helps create pathways for them to demonstrate trustworthiness, build credit, and eventually qualify for mainstream financial opportunities. Q2: Experian recently released an analysis highlighting the impact of CBA tradelines on consumer creditworthiness. What stood out to you in the findings? Dara:The data was incredibly affirming. Seeing that 70% of previously unscored consumers with a CBA tradeline reached prime or near-prime within a year highlights just how powerful inclusive credit reporting can be. It shows that when people with limited credit histories are given the opportunity to demonstrate responsible repayment, they make enormous progress. I was also encouraged by the 48-point average increase among deep subprime consumers. These gains can dramatically change someone’s financial trajectory through lower borrowing costs, access to better financial products, and more stability for their families. More broadly, this analysis reinforces what we see daily: thoughtful credit-building programs, when paired with education and support, create real and lasting change for consumers who need it most. It shows subprime consumers can perform when given the opportunities that they are often denied. Q3: From CBA’s perspective, what approaches best help financial institutions better serve underserved consumers? Dara:A major opportunity is for financial institutions to embrace alternative data that reflects consumers’ real financial lives. Data plays such a vital role in lending decisions and expanding access to fair and affordable resources; we have to modernize our approach. Many people pay their rent, utilities, and telecom bills on time every month, yet historically these payments haven’t counted toward building credit. We’ve seen incredible momentum around rent reporting, and the impact is significant –especially for people with thin or nonexistent credit histories. Rent is often a person’s largest monthly expense, and when that positive payment history is reported, it can quickly establish or improve credit. This progress has become even more meaningful with the Federal Housing Finance Agency’s approval of VantageScore 4.0 for use in mortgage underwriting. Because VantageScore 4.0 incorporates rental payment data where available, these reporting efforts can now play a more direct role in expanding fair access to homeownership for consumers who have historically been left out. In addition, programs like Experian Boost show how empowering it can be when consumers have agency over the information included in their credit files. This feature allows people to get credit for utility, telecom, streaming, rent payments and many other things they are already doing responsibly. It’s a great example of meeting consumers where they are and acknowledging financial behaviors that have historically gone unrecognized. Financial institutions should continue looking for ways to bring these types of innovations to more consumers, especially those overlooked by traditional models. Q4: From your view, how do companies like Experian help advance financial inclusion? Dara:Experian plays an essential leadership role in expanding access to credit, especially through initiatives that rethink how data can work for consumers rather than against them. They’ve been a leader in modernizing the credit reporting industry. Programs like Experian Boost are great examples of that—giving consumers the option to add positive payment information and potentially improve their credit in a matter of minutes. It’s a simple concept, but it has opened doors for millions of people who previously struggled to gain traction in the system. Similarly, Experian’s commitment to supporting rent reporting has been a major step forward. The ability for tenants to build credit through their rent payments, which is one of the most consistent household expenses, helps create equity for people who might not have access to traditional credit-building products. And on a broader level, Experian’s willingness to partner with mission-driven organizations like CBA demonstrates a shared belief that credit is a gateway to opportunity. With analytical insights like our most recent study, Experian is helping validate the importance of inclusive reporting and informing the industry about the real-world benefits for underserved communities. Q5: What misconceptions do you see about credit-challenged consumers, and what should the financial industry understand? Dara:One of the biggest misconceptions is that people with limited or poor credit histories lack financial discipline. In reality, many of them pay significant bills, including rent, utilities, childcare and more, on time every month but simply don’t receive credit for it in the traditional scoring system. Another misconception is that credit building loans or other community-based nonprofit lender products don’t make enough of a difference to report. But as this analysis shows, they absolutely do. Even a single tradeline can serve as a bridge toward greater financial stability. The industry should recognize that credit-building is a foundational tool for economic mobility, and millions of people need better access to programs that support it. My conversation with Dara reinforces what makes Credit Builders Alliance an essential component of the financial ecosystem: their work is grounded in equity, powered by community, and focused on creating lasting pathways to economic mobility. At Experian, we are proud to stand alongside CBA as a partner in expanding inclusive credit reporting, advancing responsible use of alternative data, and ensuring consumers have more control and visibility over their financial futures. The insights from our collaborative analysis make one thing clear: when people are given the chance to demonstrate their financial capabilities, they do. And together, we can make that chance available to millions more. If you’re interested in learning more about Credit Builders Alliance, their mission, and the powerful work they’re leading to expand financial opportunity, I encourage you to visit creditbuildersalliance.org. Whether you represent a nonprofit, a financial institution, or simply want to understand how credit-building strengthens communities, CBA offers resources, tools, and programs that make a meaningful difference. Together, we can continue to open doors, unlock potential, and bring financial power to all.